Tax Advantages of Homeownership: Mortgage Tax Benefits Every Tucson Homeowner Should Know

Jul 13, 2026By Derrick Polder • NMLS #207630 • Published: July 13, 2026 • Updated: July 22, 2026

Read article

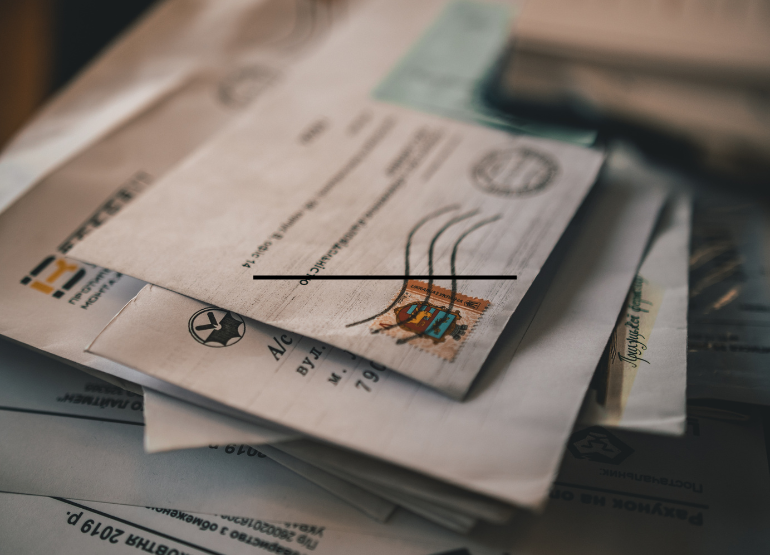

From Closing to Clutter: Navigating Post-Loan Junk Mail and Protecting Your Wallet

Closing on a home loan is an exciting milestone. Whether you've just purchased a new home and are planning your first renovation project or completed a refinance and are looking forward to improved monthly cash flow, there's plenty to celebrate.

Then the mail starts arriving.

Suddenly your mailbox is filled with offers for home warranties, security systems, mortgage protection insurance, replacement windows, and other home-related services. Many homeowners wonder how these companies got their information and whether their lender shared it.

The good news is that your mortgage lender is not selling your personal information.

At The Polder Group at CrossCountry Mortgage, protecting our clients' privacy is important to us. We do not sell borrower information to third-party marketers.

So why are you receiving these offers?

The answer lies in public records.

Once your home purchase or refinance transaction closes, the title company records your deed and mortgage documents with the county. This recording process makes certain information publicly available, which allows marketing companies to access it.

After your loan closes and the deed is recorded, the following information may become part of the public record:

Because these records are public, businesses can legally obtain the information and use it for marketing purposes. Some local companies use the data directly, while others purchase mailing lists from marketing firms that collect public records.

Unfortunately, this process cannot be prevented as it is part of the legal recording requirements associated with property ownership.

While it may be impossible to eliminate unwanted mail entirely, there are several reputable services that can significantly reduce the volume of solicitations you receive.

This service is operated jointly by the major credit reporting agencies: Equifax, Experian, Innovis, and TransUnion.

You can use it to opt out of:

Homeowners can opt out for five years or permanently at no cost.

DMAchoice allows consumers to reduce direct marketing mail by selecting categories they no longer wish to receive.

Common categories include:

A small fee applies, and your preferences remain active for up to 10 years.

Catalog Choice is a nonprofit organization that helps consumers stop unwanted catalogs and certain promotional mailings.

The service is free, although donations are welcomed to support its mission.

PaperKarma is a mobile app available for iOS and Android devices that helps users remove their names from mailing lists.

The service offers a trial period followed by subscription options for continued use.

Not all mail you receive after closing is junk.

Many important documents may arrive during the weeks following your loan closing, including:

Before shredding any mail, take a moment to review it carefully to avoid missing important information regarding your home or mortgage.

Some mail pieces are designed to look official and may create confusion about whether additional action is required.

Common examples include:

Some companies send solicitations offering copies of your recorded deed for a fee.

Remember, your deed recording fees were already handled during closing. If you have questions about your recorded documents, contact your title company directly.

You may receive offers suggesting that mortgage protection insurance is required.

These products are generally optional. If you're interested in protecting your family financially, speak with your insurance professional about available life insurance or mortgage protection options.

Some companies charge fees to set up biweekly or semi-monthly mortgage payment plans.

Before paying for these services, contact your loan servicer directly. Many servicers can help you establish alternative payment arrangements at little or no cost. You may also be able to set up automatic payment options through your bank.

At The Polder Group at CrossCountry Mortgage, we want your homeownership experience to be as smooth and stress-free as possible.

If you receive a piece of mail that references your mortgage and you're unsure whether it's legitimate, don't hesitate to reach out. Our team is happy to help you determine whether the communication is important or simply a marketing solicitation.

Whether you're buying your first home, refinancing, or exploring your financing options, our team is here to guide you every step of the way. Learn more about our mortgage services on our <a href="https://www.thepoldergroup.com/buy">Home Buying page</a>, explore available <a href="https://www.thepoldergroup.com/mortgage-loan-programs-tucson">Loan Programs</a>, or <a href="https://www.thepoldergroup.com/contact-tucson-mortgage-team">contact us</a> with any questions.

Yes. Once your property transaction is recorded, certain information becomes public record, making it accessible to businesses that market home-related products and services.

No. Reputable lenders do not sell borrower information for these purposes. Most of the mail comes from companies using publicly available property records.

While it may not be possible to stop every solicitation, services like OptOutPreScreen, DMAchoice, Catalog Choice, and PaperKarma can significantly reduce unwanted mail.

Review all mortgage-related correspondence carefully. If you're unsure whether a notice is legitimate, contact your mortgage servicer, title company, or loan officer before responding or making any payment.

This article is for educational purposes only and does not constitute financial or mortgage advice. Loan programs, rates, and guidelines may change at any time. All loans are subject to credit approval and underwriting. For guidance tailored to your situation, consult a licensed mortgage professional.

By Derrick Polder • NMLS #207630 • Published: July 13, 2026 • Updated: July 22, 2026

Read article

By Derrick Polder • NMLS #207630 • Published: July 13, 2026 • Updated: July 22, 2026

Read article

By Derrick Polder • NMLS #207630 • Published: July 9, 2026 • Updated: July 17, 2026

Read article

By Derrick Polder • NMLS #207630 • Published: Original Publication Date 6.22.26 • Updated: June 30, 2026

Read article

Different levels of commitment - all start with a conversation.

A quick first step to review loan options and next steps with a local expert.

Ready to move forward now? Secure application - Credit review required

Not ready for a form? Ask a question and a local expert will follow up.